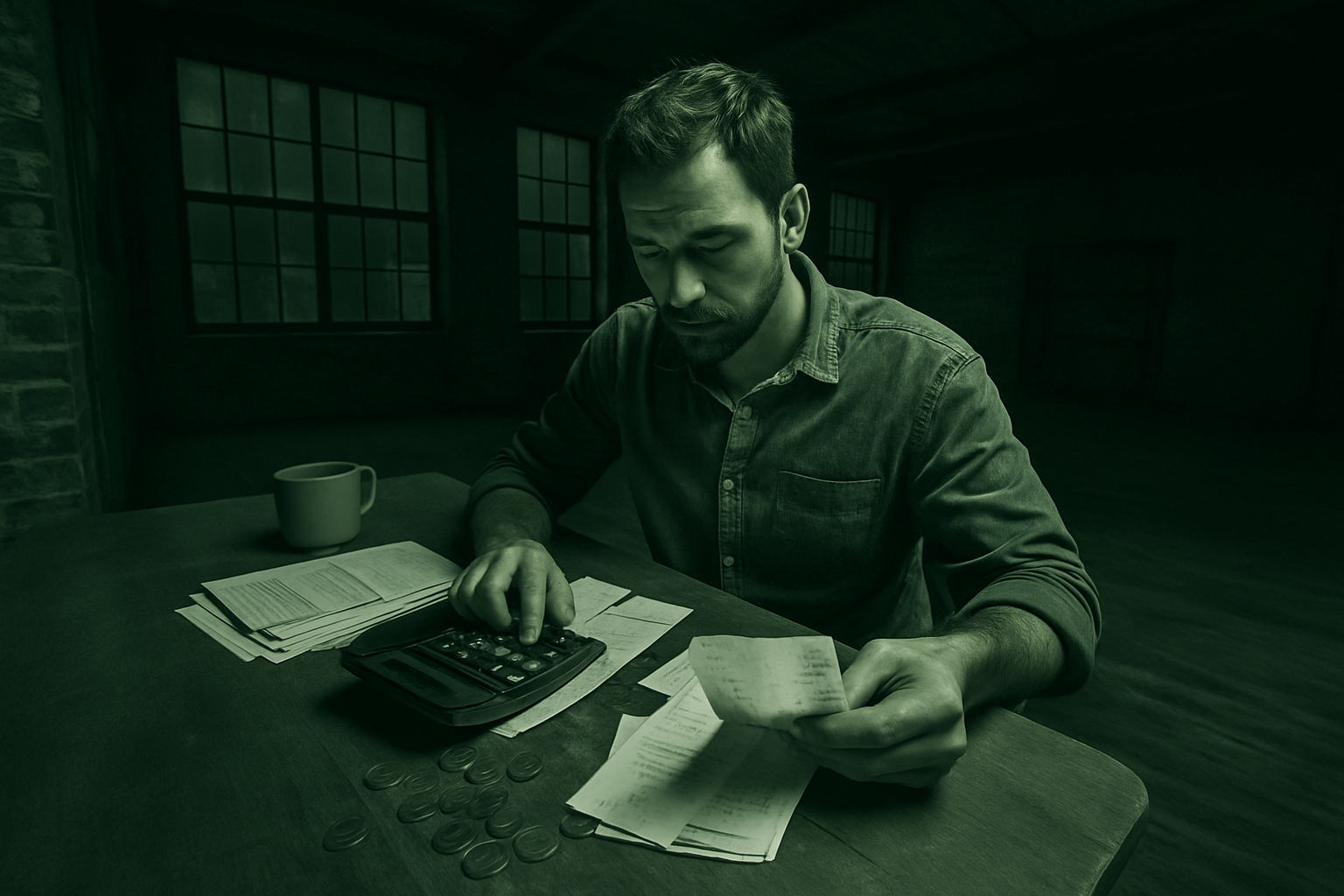

Get Clear on Your Money Flow

Before you can manage your money, you need to know where it’s going. Track every dollar literally. What’s coming in each month? What’s going out? Don’t guess. Don’t round up or down. Just get the numbers. It doesn’t matter if you use a money app, a spreadsheet, or a cheap notebook from the drugstore what matters is that you pick a system and stick with it.

Start with your fixed expenses. These are the non negotiables: rent, utilities, transportation, debt payments. They should be the first things accounted for in your monthly flow. Once they’re covered, you’ll have a clear view of what’s left.

Then it’s time to plug the leaks. Scroll through your transactions and highlight the stuff you forgot you even paid for subscriptions you barely use, impulse buys, low impact spending that’s draining cash without adding anything worthwhile. Small changes here create breathing room fast.

Get intentional. Your money should be working for you, not slipping through the cracks.

Set a Monthly Money Date

Pick one day a month same day, every time and block it off. No multitasking, no rescheduling. This is your check in, not a full budget overhaul. Thirty minutes is plenty.

Start by looking at last month’s numbers. What worked? What didn’t? Maybe you overspent on takeout but killed it with your grocery budget. No guilt just data. Use it.

Next, scan the month ahead. Got a trip planned? A quarterly bill hitting? Income slower this month? Adjust your spending buckets now, before you’re scrambling.

Keep it short, tight, and honest. If it feels like a burden, you won’t keep doing it. The goal isn’t perfection. It’s consistency. One small habit that keeps your money grounded in your actual life.

Skip the finance drama. This is just routine maintenance like brushing your teeth, but for your budget.

Automate What You Can

Simplify. That’s the whole point here. Automation takes human error and procrastination out of the equation. First move: set up an auto transfer to your savings the second your paycheck lands. Even if it’s just $50, consistency beats ambition.

Next, get your recurring bills rent, phone, insurance on autopay. One time setup, ongoing peace of mind. No more late fees, no more oops I forgot days.

Then there’s your spending money. Use digital envelopes or budget buckets for categories like groceries, dining out, and takeout. It gives you permission to spend within limits. Automation won’t solve money problems overnight, but it builds a system that runs even when you’re busy, tired, or just not in the mood to think about it.

Set it up once. Let it work in the background. Just check in monthly to adjust the dials.

Plan for the Expected and the Unexpected

Some expenses don’t show up every month, but you know they’re coming car repairs, holiday gifts, plane tickets. That’s what a mini “buffer” account is for. Think of it as your personal shock absorber. You don’t need to overbuild it, just keep it alive. Toss in a small, set amount each month and let it quietly do its job.

Next, the emergency fund. Start small $10 is fine. It’s about consistency and developing the muscle. The point is to have something when things blow up a layoff, a broken laptop, whatever. What matters more than the amount is that you actually start.

Finally, don’t forget to plan for the good stuff. A vacation, a kitchen renovation, clearing that lingering student loan these are financial goals worth aiming for. They’re motivators. They give your monthly routine some edge and purpose beyond survival. Want to make the routine stick? Tie it to something you’re excited about.

Pay Off Debt Strategically

Start with your most expensive debt. That usually means credit cards. The interest rates are brutal and compound fast, so even small payments toward that balance can save you big over time. It’s tempting to spread money across every debt, but focus firepower where it hurts most. Pay minimums on everything else until the high interest stuff is under control.

Check your progress once a month no judgment, just data. If you got off track, tweak the plan. If you crushed it, double down. Debt payoff isn’t linear. Some months are tight, others let you do more. Stay realistic, stay flexible.

Also, understand the kind of debt you’re carrying. Not all of it’s bad. A mortgage might build equity. A student loan could be investing in your future. But a maxed out department store card? That’s a drag on your goals. Know the difference so you don’t waste energy on the wrong battles.

For more on that, check out: Understanding Good vs. Bad Debt in Your Daily Life.

Keep It Flexible, But Non Negotiable

Financial routines aren’t carved in stone and they shouldn’t be. Life throws curveballs: job changes, medical bills, surprise opportunities. Your monthly money plan should be able to bend without breaking.

Adapt Without Abandoning Your Routine

If your income shifts or expenses spike, adjust quickly but stay engaged.

Reassess categories like entertainment, subscriptions, or savings contributions as needed.

Flexibility doesn’t mean inconsistency. It means rebalancing when the numbers do.

Momentum Over Perfection

You won’t get everything right every month, and that’s okay. The goal is to show up consistently.

A misstep doesn’t erase progress learn and move forward.

Progress is measured in small, repeated actions not big, perfect months.

Good enough and sustained beats perfect and abandoned.

Don’t Skip the Check Ins

These monthly reviews might feel minor, but over time, they deliver major results.

Even a 15 minute check in keeps your financial awareness sharp.

Spotting patterns early = fewer crises later.

A small commitment now compounds into long term confidence with your money.

Make This the Year It Sticks

Stop Winging It

If you’ve been relying on guesswork or last minute budgeting, 2026 is the year to turn that around. Financial stability isn’t about earning more it’s about paying attention and building systems that are repeatable and realistic.

Budgeting doesn’t need to be complicated to be effective

Small, consistent actions beat occasional big efforts

Focus on systems you can stick with when life gets busy

Build a Routine That Works for You

The best financial routine is one that fits your lifestyle, energy, and priorities. Whether that means a color coded spreadsheet, a weekly voice memo check in, or an app that runs in the background make it yours.

Choose tools that align with your habits (not fight against them)

Start with 15 30 minutes a month dedicated to finances

Adapt the system instead of abandoning it when things shift

Align Your Budget With Your Values

Money is not just about numbers it’s a reflection of what matters to you. When your spending and saving habits match your goals and values, financial routines stop feeling like a chore and start becoming empowering.

Does your budget reflect what you truly care about?

Are you making space for both essentials and the meaningful extras?

Own your financial decisions with clarity and confidence

2026 can be the breakthrough year you stop managing your money reactively and start doing it with intention. Set the tone now and future you will thank you.